PJAIT AI Summit 2026: Dragan, Dukaj, and Naskręcki on the Future of Artificial Intelligence

Blockchain is one ofthe most important inventions of the 21st century in the digital economy. The technology, which emerged alongside Bitcoin in 2009, extends far beyond purely financial applications. Today, blockchain forms the foundation of Web 3.0 (Web3), a new vision of the internet in which decentralization, security, and transparency become global standards.

Blockchain is more than just the technology underlying Bitcoin. Blockchain isa decentralized, distributed database that stores information in the form of a chain of cryptographically linked blocks. Each block contains a set of transactions or data, a timestamp, and a reference to the previous block (called a hash), thereby creating an immutable chain.

This structure ensures that none of the previous blocks can be altered without recalculating the entire chain—which makes the blockchain an extremely secure system.

A key feature of blockchain is itsdecentralized nature. Instead of storing data on a single, central server (like traditional databases), blockchain distributes information across thousands of computers (nodes) around the world. Each node stores a complete copy of the blockchain, which means there is no single point of failure and no entity can unilaterally manipulate the data.

Blockchain security is based on advanced cryptography, particularly hash functions and digital signatures. Each block is identified by a unique code (hash) generated from its contents using a cryptographic algorithm (most commonly SHA-256).

This means that even the slightest change to a block’s data (the block’s contents—records, transactions, etc.) will alter its hash into a completely different string of characters, immediately signaling a threat to integrity.

In addition, blockchain uses public-key cryptography, which allows users to securely sign transactions with their private key, while others can verify the authenticity using their public key. This combination makes blockchain virtually immune to unauthorized access and data tampering.

For a blockchain to function without a central—let’s call it—authority, it needs a way for all nodes in the network to agree on which transactions are valid.

This is where consensus mechanisms come into play—led by Proof of Work and Proof of Stake.

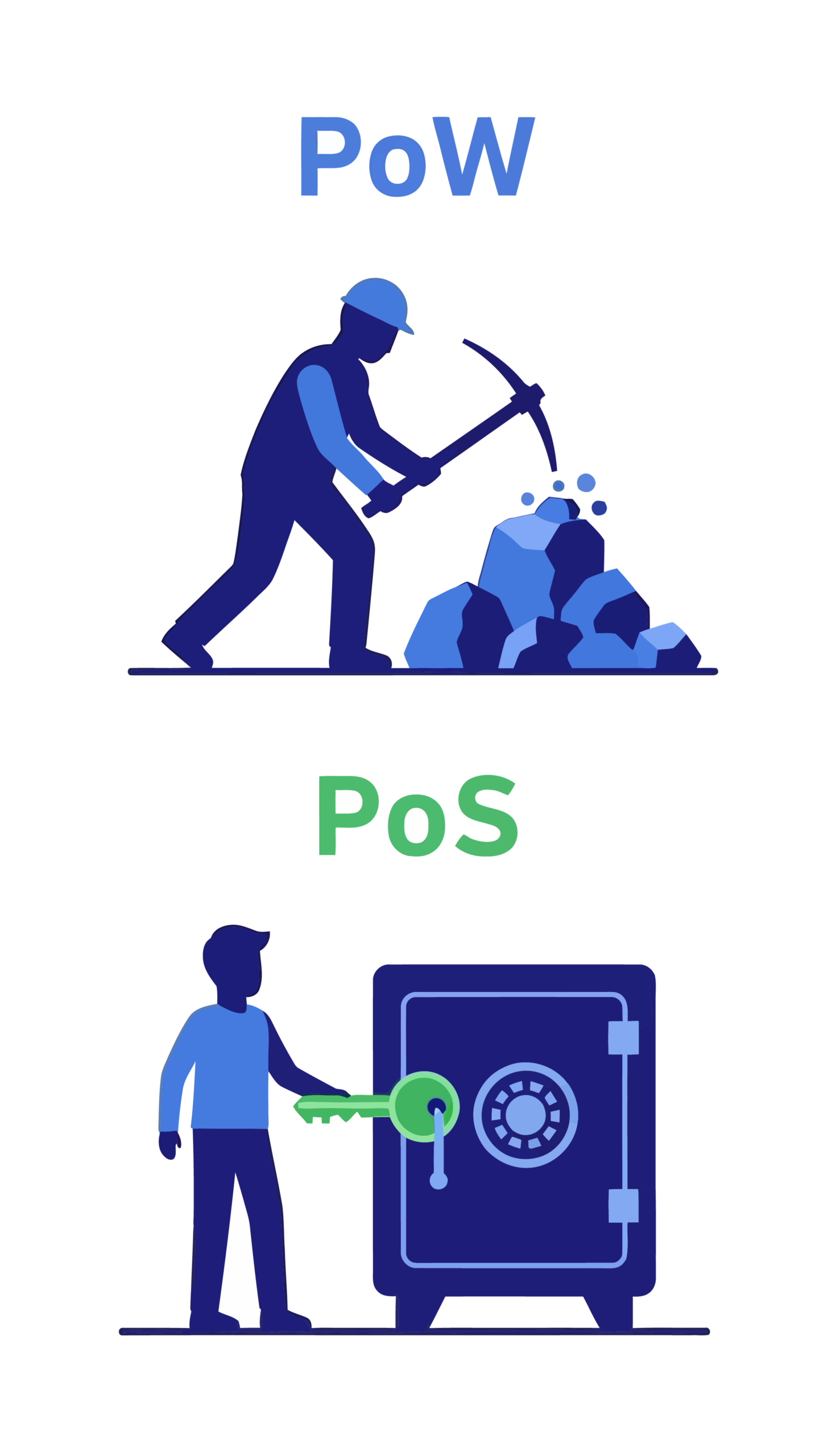

Proof of Work (PoW) is an algorithm in which network participants (known as miners) compete to solve complex mathematical problems (such as finding a block hash with a specific number of leading zeros) in order to earn the right to add a new block to the chain. The winner receives a reward in the form of new cryptocurrency coins. This method is secure but very energy-intensive—hence the controversy surrounding Bitcoin’s impact on the environment.

Proof of Stake (PoS), on the other hand, is a more modern approach in which participants (validators) secure the network by staking their cryptocurrency. Instead of energy-intensive computations, a validator is selected in proportion to the size of their stake. This method is significantly more energy-efficient and has become the standard in many new blockchain projects, including Ethereum 2.0.

Bitcoin, introduced in 2009 by a mysterious figure (or group) known as Satoshi Nakamoto, was the first practical implementation of blockchain. It serves primarily as a digital currency and store of value, often referred to as “digital gold.” Bitcoin thus introduced the concept of money that does not require intermediaries (such as banks or governments) and is secured by cryptography rather than trust in institutions.

Ethereum, launched in 2015, went much further—rather than being merely a payment system, Ethereum is a fully-fledged decentralized computer capable of executing complex programs known as smart contracts. This feature has opened up unlimited possibilities for blockchain applications, ranging from decentralized finance (DeFi) to the tokenization of physical assets.

Blockchain and decentralization are, in fact, the cornerstones of the next generation of the internet, Web 3.0. While Web 1.0 (the 1990s) was static, and Web 2.0 (the 2000s) introduced interactivity and social media (but under the control of large corporations), Web 3.0 puts control and ownership of data back in the hands of users.

In the Web3 ecosystem, users control their own data and digital identities, rather than sharing them with platforms. The token economy allows users to earn income by participating in networks, and smart contracts automatically enforce agreements without the need for intermediaries. This decentralization has thus reduced dependence on monopolistic technology platforms.

Decentralized finance (DeFi), which enables lending and investing without the involvement of traditional banks. Protocols such as Uniswap, Aave, and Compound offer banking services through smart contracts that anyone can interact with.

DeFi thus primarily eliminates intermediaries (banks that charge fees), time constraints (it’s open 24/7), and extensive credit requirements (cryptocurrency collateral is sufficient).

Blockchain is also ideal for tracking goods throughout the supply chain. Every step—from production to transportation, storage, and delivery—can be recorded on the blockchain, creating an immutable and transparent record.

This helps verify the authenticity of products (combating counterfeiting), track the origin of goods (particularly important for organic and ethically sourced products), and automate payments using smart contracts (once the goods reach their destination, the payment is automatically released).

Blockchain enables prosumers (people who generate energy, e.g., using solar panels) to sell their surplus energy directly to other consumers, bypassing energy suppliers.

Smart contracts can automatically record energy production and consumption, settle accounts between parties, and manage energy distribution in smart grids. This could shift the energy sector toward greater decentralization and efficiency.

A traditional identity management system is centralized. Within this system, various institutions—such as banks, government agencies, and service providers—store and process our data. This creates a number of risks, such as those caused by a single system being hacked, which could result in all of our data being stolen and used in cyberattacks.

Blockchain enables decentralized identity management. Instead of relying on a central authority, our identity can be stored in a digital wallet on the blockchain. This allows us to share only the data we want for a specific purpose—for example, to verify our age without revealing our full name.

This benefits both organizations—which can collect less data, thereby reducing the risk of cyberattacks—and users, who gain full control over their identity and a reduced risk of data theft.

Smart contracts, as programs running on the blockchain, can also be used in:

Tokenization is the process of converting a representation of value (whether it be money, stocks, real estate, or art) into a token on a blockchain.

This gives us the opportunity to own a fraction of an asset (e.g., 1% of a building or a work of art), to facilitate trading in assets that were previously illiquid (e.g., real estate or art), and to gain greater access, allowing us to invest in assets that previously required a large initial capital outlay.

Although blockchain and artificial intelligence are sometimes viewed as separate technologies, their combination is now one of the key trends in technology.

Large language models (LLMs) based on transformers require massive amounts of high-quality data for training. This is where blockchain comes in, as it can ensure that the data used to train LLMs has not been altered, is authentic, and comes from reliable sources. In a world where deepfakes and information manipulation are becoming an increasingly serious problem, such a guarantee is of paramount importance.

Furthermore, decisions made by AI systems (especially those based on LLMs) can be recorded on the blockchain, creating an auditable trail of every recommendation, classification, or action. This is particularly important in medical, legal, or financial applications.

Going even further, in the context of Big Data—where data is now the driving force behind the digital economy—blockchain enables data creators and owners to monetize their datasets without intermediaries. Individuals can be rewarded for sharing data to train large language models (LLMs) while retaining control over it.

This convergence of blockchain, big data, and large language models creates an ecosystem where data is secure and backed by responsible AI, and creators are fairly compensated for their work.

For those who would like to delve deeper into the world of blockchain, Web3, and related technologies, education is key. The computer science program computer science PJAIT provides a solid foundation in programming, mathematics, and software engineering—everything needed to build blockchain applications. The program includes specializations in artificial intelligence, distributed systems, and data science, which are closely linked to blockchain and the future of Web3, and provide a thorough understanding of both the technical and economic aspects of decentralized systems.

Despite its enormous potential, blockchain faces numerous challenges. Bitcoin and Ethereum can process only a dozen or so transactions per second—while new solutions (Layer 2, sharding) are attempting to address the scalability issue, this remains an area of active development.

For businesses, the adoption of blockchain requires a clear legal framework, a process that is not made any easier by governments around the world, which are struggling to regulate blockchain and cryptocurrencies.

Security is also a significant factor here; although blockchain is cryptographically secure, human error (such as losing a private key) and errors in smart contracts can lead to the loss of funds.

After all, energy consumption is also a major challenge, especially with the PoW algorithm. While we now have the more energy-efficient PoS, this only mitigates the problem—it doesn’t solve it.

Blockchain is a groundbreaking technology that is transforming the way we store data, verify ownership, automate contracts, and build decentralized systems. From DeFi to identity management, and from smart contracts to tokenization, blockchain has the potential to reshape virtually every sector of the economy.

Web 3.0 represents a shift away from a centralized model of the internet toward a decentralized one, in which users have control over their data and earnings. It is a bold vision, sometimes controversial, but certainly one that cannot be ignored.